")

In this Article, we dive deep into the recent quarterly financial report of Cann Group Limited, an emerging leader in the Australian cannabis market. Our analysis seeks to unravel the dual narrative of promising growth against a backdrop of escalating debt and financial maneuvering.

Revenue Growth and Operational Advancements

Cann Group reported a noteworthy uptick in revenue for the quarter ending December 2023. Consolidated sales for December stood at $1.28 million, contributing to a quarterly revenue of $4.46 million. This marks a commendable 16% increase compared to the same period last year. The year-to-date revenue figure of $8.49 million, a 46% surge from the previous year, paints a picture of a company on a rapid growth trajectory.

Operationally, the company has made significant strides. The December quarter saw the implementation of full-scale production, reflecting Cann Group’s commitment to enhancing product quality and broadening its product range. The development of high-THC cultivars and the adoption of improved production techniques signal a robust operational strategy in tune with market demands.

Breakdown of Operational Expenses

Cann Group’s operational expenses are a composite of various key components, each contributing to the company’s cash outflow:

Product Manufacturing and Operating Costs: With expenses amounting to $3.66 million for the quarter, this is a significant outflow. These costs cover everything from the production of cannabis products, quality control, to compliance with regulatory standards. Given the stringent requirements in the cannabis industry, these costs are substantial but essential for maintaining product standards and market competitiveness.

Staff Costs: The company spent $3.635 million on staff costs in the same period. This figure highlights the labor-intensive nature of the cannabis industry, where skilled labor is crucial for research, cultivation, and management. While high, these costs are indicative of the company’s investment in human capital, essential for innovation and operational excellence.

Administration and Corporate Costs: At $1.117 million, these costs encompass the necessary overheads for running the company, including office expenses, legal and professional fees, and other administrative activities. These are vital for the day-to-day operations and strategic management of the company.

Significance of the R&D Tax Rebate

The R&D tax rebate plays a pivotal role in Cann Group’s financial ecosystem. For the quarter, the rebate amounted to $3.468 million, a substantial figure that significantly impacts the company’s cash flow.

Impact on Net Cash Flow: Without this rebate, Cann Group’s net cash used in operating activities would be markedly higher. The rebate effectively offsets a considerable portion of the operational costs, providing much-needed financial relief.

Implications of Reliance on the Rebate: Relying on the R&D tax rebate introduces an element of risk and uncertainty. While it currently provides a financial cushion, changes in government policies or eligibility criteria could alter this scenario. The loss or reduction of this rebate could significantly strain the company’s cash flow, necessitating a reevaluation of its operational and financial strategies.

Increasing Debt Levels

While the revenue and operational advancements are encouraging, they are contrasted by the company’s increasing reliance on debt. During the quarter, Cann Group withdrew $4.37 million from its Working Capital Facility and drew down an additional $1.08 million from its Construction Facility for the Mildura development. This points to a growing dependency on external financing to fuel its expansion plans.

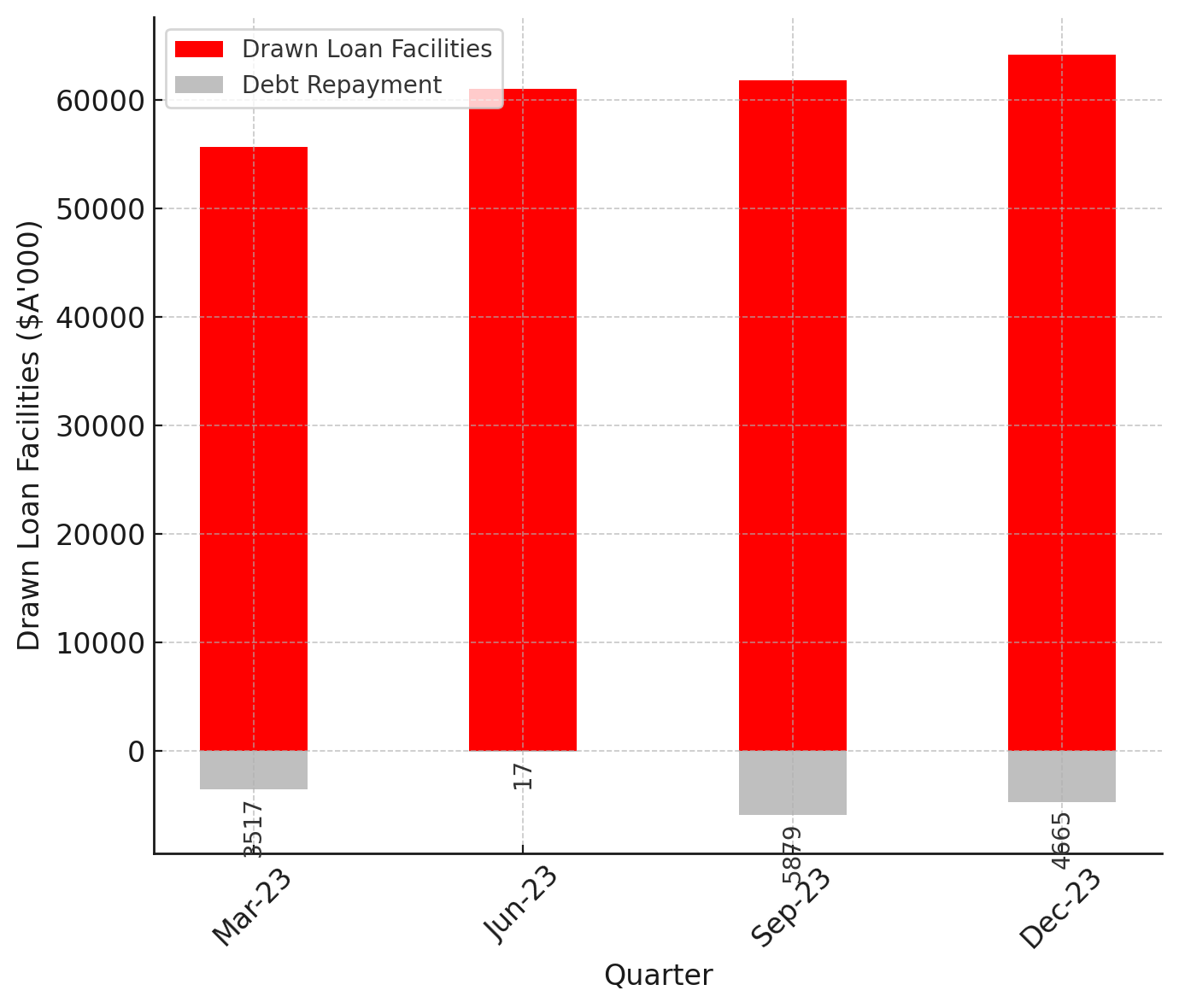

As of the quarter end, Cann Group’s debt situation is characterised by significant figures. The total facility amount stood at a substantial $67.305 million, with an amount of $64.078 million drawn at quarter end. This reveals a stark reality: despite making considerable debt repayments totaling $14 million over the last four quarters, the company’s current debt level has escalated by nearly $10 million compared to the previous year.

Quarterly Escalation of Financial Leverage Despite Debt Repayment Efforts

Here, we see the trend of increasing debt levels over recent quarters. The graph shows the rise in debt despite repayment efforts, emphasising the growing financial leverage the company is undertaking.

On one hand, Cann Group is experiencing tangible growth in revenue and is making significant operational advancements. On the other, there is a clear and present challenge posed by its increasing debt levels and the reliance on external financing. This dichotomy is at the heart of Cann Group’s current financial narrative and is crucial for stakeholders to understand.

The Debt Dilemma: Unpacking Cann Group’s Escalating Financial Obligations

A critical aspect of Cann Group Limited’s financial narrative that demands attention is its burgeoning debt situation. Despite significant debt repayments, the company’s debt levels have alarmingly risen. This section aims to dissect the reasons behind this increase, its implications for the company, and the potential impact on shareholders.

Why Debt Levels are Rising

Growth-Driven Financing: Cann Group’s increasing debt is primarily attributable to its aggressive growth strategy. Investments in expanding production capacity, research and development, and market diversification require substantial capital. The company has been leveraging debt financing to fuel these growth initiatives, leading to an increase in its overall debt burden.

Capital Expenditures: The development of the Mildura facility and advancements in production technology have necessitated significant capital outlays. These expenditures, while crucial for long-term growth, have contributed to the rising debt as the company opts for debt financing to cover these costs.

Operational Cash Burn: Cann Group is still in a phase where its operational expenses and investments outpace its revenue generation. This cash burn situation necessitates the need for external financing, contributing to the increase in debt levels.

Implications for Cann Group

With rising debt comes reduced financial flexibility. The company’s ability to respond to market changes or pursue new opportunities may be constrained by the need to prioritise debt servicing and management. Increasing debt levels lead to higher interest obligations. This can put pressure on the company’s cash flows, particularly if revenue growth does not accelerate accordingly. There is a risk of over-leverage, where the company might find itself in a position of having more debt than it can comfortably manage, especially if there are any downturns in the market or operational setbacks.

Impact on Shareholders

Increasing debt can be a red flag for investors, potentially leading to a decrease in stock value. Investors often view high debt levels as a sign of increased risk, which can affect the stock’s attractiveness. The company’s strategy to manage debt through equity dilution by issuing more shares can adversely affect existing shareholders, reducing their ownership percentage and potential returns.

Cann’s Risky Financing Strategies

The Implications of Issuing More Notes

Issuing additional debt in the form of notes is a strategy that provides Cann Group with immediate capital. This can be crucial for sustaining operations, funding growth initiatives, or meeting existing financial obligations. However, this approach also increases the company’s debt burden, leading to higher interest obligations in the future.

A heightened debt level can strain the company’s cash flows, especially if revenue growth does not keep pace with the increasing financial obligations. This could potentially lead to a situation where the company’s earnings are primarily directed towards servicing debt, leaving little for reinvestment or distribution to shareholders.

Converting Discounted Shares

Cann Group’s strategy of converting discounted shares presents another set of challenges. While this approach provides a mechanism to raise capital without incurring additional debt, it comes with the risk of equity dilution. Equity dilution occurs when a company issues new shares, reducing the ownership percentage of existing shareholders.

This dilution can have several consequences:

Decrease in Earnings Per Share (EPS): As more shares are issued, the company’s earnings are spread over a larger number of shares, potentially lowering the EPS. A lower EPS can make the stock less attractive to investors.

Impact on Stock Price: The introduction of additional shares in the market, particularly at a discounted rate, can put downward pressure on the stock price. This is often exacerbated if these shares are rapidly sold, a phenomenon referred to as “dumping” on the market.

Investor Confidence: Frequent equity dilution can erode investor confidence. Investors may perceive such actions as a sign that the company is struggling to finance its operations through more sustainable means.

Future Outlook and Scenarios

Optimistic Scenario: Successful Debt Management and Revenue Growth

In a positive turn of events, Cann Group successfully manages its debt burden while simultaneously driving robust revenue growth. This scenario envisions the company making strategic decisions that optimise its operational efficiencies, reduce production costs, and significantly boost sales, particularly in new and emerging markets.

The successful expansion of its product line, coupled with favorable regulatory changes in the cannabis industry, and a continuation of the R&D tax rebate could provide additional tailwinds. As revenue streams strengthen, the company becomes more self-sufficient, reducing its reliance on debt financing and improving its overall financial health. For shareholders, this scenario offers the prospect of sustainable growth and potentially attractive returns.

Pessimistic Scenario: Continued Debt Escalation and Equity Dilution

Conversely, if Cann Group continues down a path of increasing its debt without a proportional increase in revenue, it risks entering a state of over-leverage. In this scenario, the company’s debt servicing obligations might outpace its earnings, leading to cash flow pressures and potential liquidity challenges.

The continued issuance of more notes and conversion of discounted shares could lead to further equity dilution, negatively impacting stock value and investor confidence. If unchecked, this could spiral into a vicious cycle, diminishing the company’s attractiveness to both current and potential investors.

Furthermore, if the R&D tax rebate is reduced or abolished, Cann Group will face an uphill battle to sustain its operational expenditures which are currently far outpacing inward cash flow.

Financial Disclaimer

This article is for informational purposes only and is not intended as financial advice. Investment decisions, particularly in volatile markets like the cannabis industry, carry risks and should not be based solely on the information provided here. We advise consulting a financial professional before making any investment choices. The author and publisher bear no responsibility for any financial outcomes resulting from decisions based on this article’s content.

{kind=link}